The 4-Quadrant System is more than just a budget; it is a complete financial framework designed to bring financial clarity to your everyday life. Most people do not struggle with money because they earn too little. They struggle because everything feels unstructured. Money moves in and out without a clear plan, leaving you wondering where it all went.

This 4-Quadrant System gives every dollar a defined space so you always know where your money goes and what it supports. Savings, Essential spending, Lifestyle spending, and Impulse spending each sit in their own quadrant. Once you organize your finances this way, your entire money picture becomes easier to understand and control.

Use this post as your starting point. Learn the quadrants and you gain a clear view of your financial life.

To explore the Quadrant Application directly, click here

To know more about the working of 4-Quadrant System, click here

Table of Contents

1: Why a Quadrant System Beats Traditional Budgeting

Budgets often fail because they expect perfection. The 4-Quadrant System works because it keeps things simple, realistic, and built around how people actually behave with money.

1. It cuts down decision fatigue.

Every purchase fits into one of four quadrants. You place it, you move on, and your system stays intact.

2. It mirrors real spending patterns.

Most people do not operate with endless categories. They operate with a few core habits. The quadrants match those habits, which makes the system easy to stick with.

3. It removes financial guilt.

Lifestyle and Impulse quadrants exist intentionally, so fun spending has boundaries instead of shame.

4. It gives instant clarity.

Four quadrants reveal your habits fast. You can see where your money supports you and where it drains you.

5. It creates consistency.

Structure beats willpower. The quadrants guide your decisions even when life gets chaotic.

This is why the 4-Quadrant System works. It makes money management simple, predictable, and stress free.

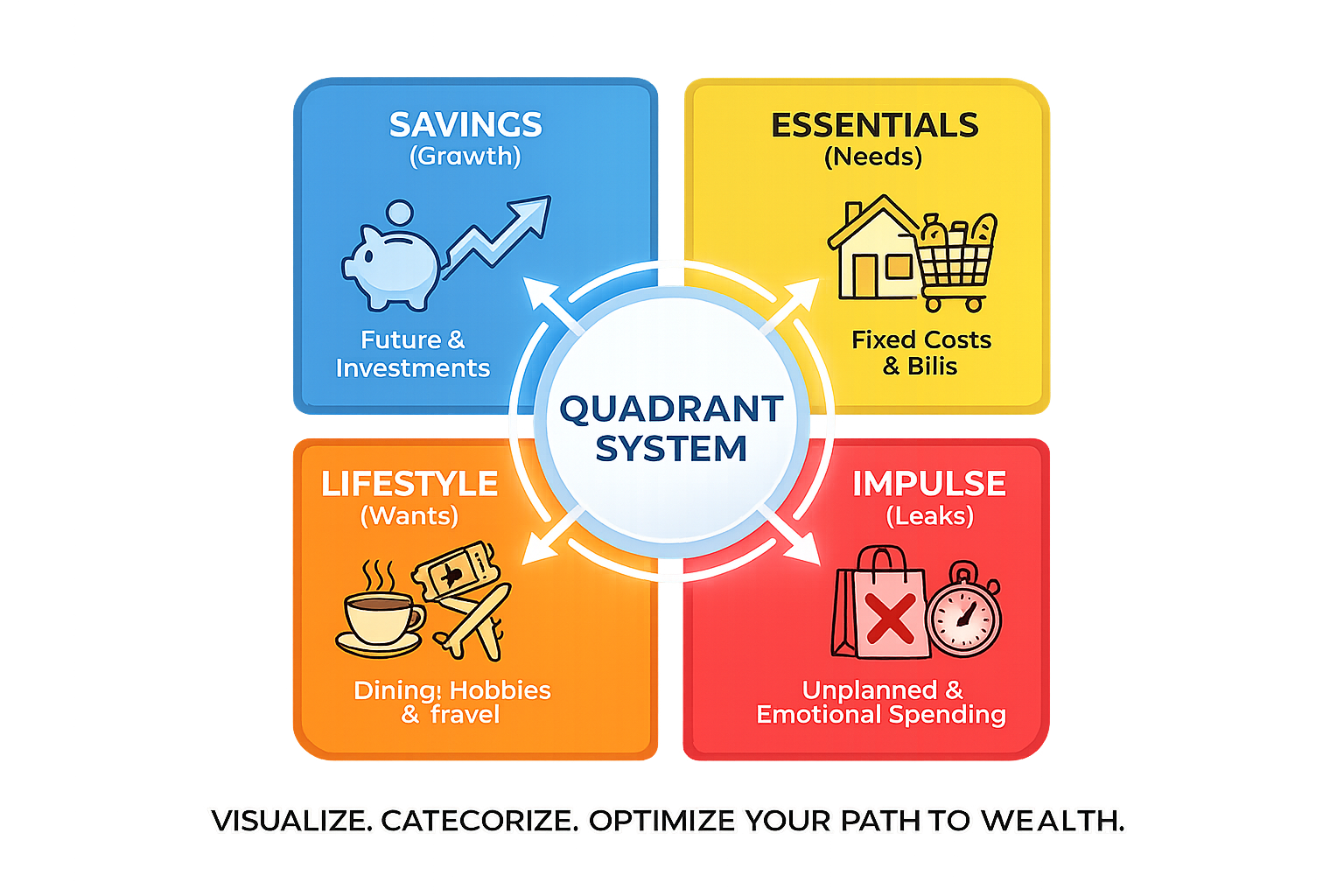

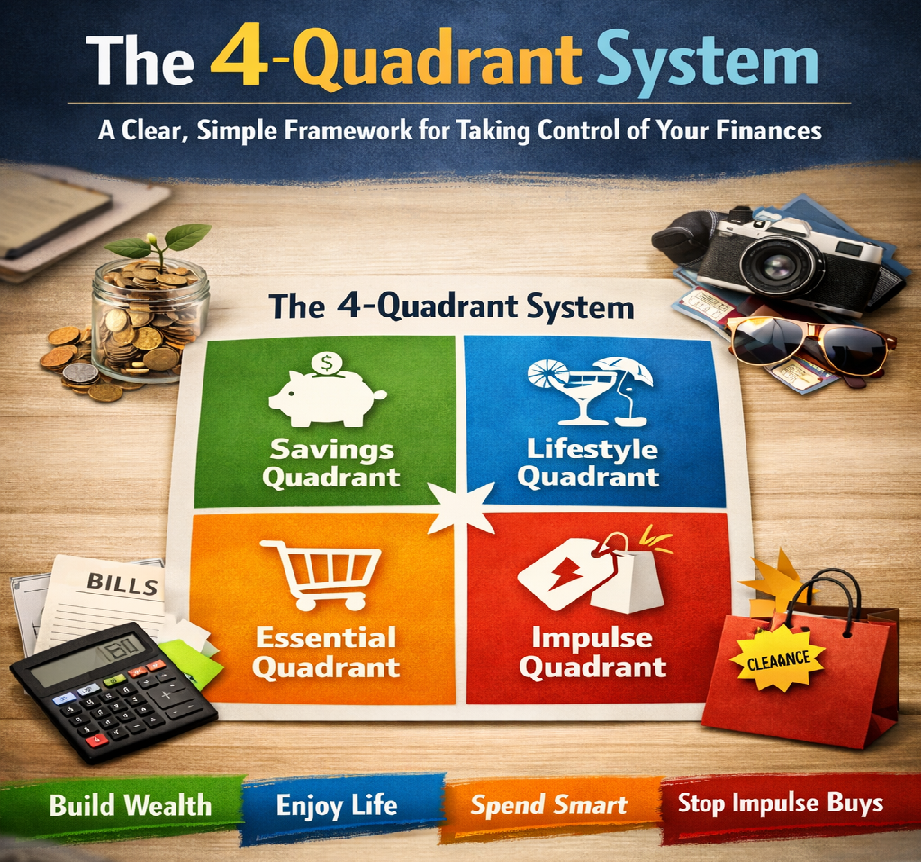

2: The 4 Quadrants and What They Mean

The strength of the 4-Quadrant System comes from its simplicity. Every dollar you spend or save fits into one of four clear quadrants. Each one has a role, a purpose, and a boundary. Once you understand these quadrants, you understand your entire financial flow.

Quadrant 1: Savings

This is your safety net and your future. It includes your emergency fund, long term savings, debt payoff, and investing. Money placed here builds stability and creates options later in life. It is the quadrant that protects you when things go wrong and rewards you when things go right. (Read more….)

Quadrant 2: Essential Spending

These are the non negotiables that keep your life stable. Housing, groceries, transportation, insurance, medical needs. This quadrant covers everything required for daily living. When you keep Essentials under control, your entire financial system stays steady. (Read more….)

Quadrant 3: Lifestyle Spending

This quadrant holds the wants that make life enjoyable. Restaurants, hobbies, entertainment, wellness, travel. Lifestyle spending improves your day to day experience and should be planned, not judged. When this quadrant is balanced, you enjoy your life without sabotaging your goals. (Read more….)

Quadrant 4: Impulse Spending

These are the spontaneous buys. The little cravings, conveniences, and quick decisions that can stack up fast. You do not eliminate this quadrant. You simply put guardrails around it so impulses stay fun instead of destructive. (Read more….)

Together, these four quadrants create clarity. They reduce guilt by giving every type of spending a defined home. You stop guessing where your money went, because the system shows you. You stop feeling bad about spending, because you can see exactly how it fits into your financial plan.

3: How to Set Up Your 4-Quadrant System in Under an Hour

Getting your 4-Quadrant System in place does not require complicated software or endless tracking. You can set it up in under an hour with a simple process that shows you exactly where your money is going and how to take control of it.

1. Track the last 30 days of spending.

Pull your bank statements or your spending app. You only need one month to see your habits clearly.

2. Label each purchase under one of the four quadrants.

Savings. Essential spending. Lifestyle spending. Impulse spending. Place each transaction where it belongs. Be honest. No judgment.

3. Calculate your natural percentages.

Add up each quadrant’s total and divide by your monthly income. This shows how you are actually using your money right now.

4. Set target percentages that reflect your goals.

Decide where you want your money to go. Increase Savings if you want more stability. Tighten Impulse if you feel out of control. Shape the system around your real priorities.

5. Build a monthly automation plan for Savings and Essentials.

Automate transfers, bills, and debt payments. These two quadrants run best when the system handles them, not your memory.

6. Create weekly spending limits for Lifestyle and Impulse categories.

These quadrants benefit from lighter, more flexible boundaries. Weekly limits keep you aware without killing the fun.

7. Schedule a one hour monthly review.

Look at your progress, adjust your targets, and reset your spending for the next month. This keeps the system alive and accurate.

Once these steps are in place, your Quadrant System runs almost on autopilot. It becomes a simple structure that guides your spending, protects your goals, and makes managing money far easier.

4: The Financial Mistakes This System Protects You From

Most money problems come from small habits that slip under the radar. The 4-Quadrant System exposes these habits and stops them before they drain your income. These are the mistakes it protects you from.

1. Treating Lifestyle purchases as Essentials.

Going out to eat is not the same as buying groceries. Upgrading your phone case is not the same as paying your phone bill. Mixing these categories hides overspending and makes Essentials look higher than they really are. The quadrants separate needs from wants so you see the truth fast.

2. Pretending Impulse spending does not count.

Quick snacks, convenience fees, small online buys. These feel harmless, but they add up. The Impulse quadrant forces these purchases into the open so you can manage them with light guardrails.

3. Saving last instead of first.

Most people save whatever is left over at the end of the month. That number is usually zero. The Quadrant System treats Savings as a core category, not an afterthought, so you prioritize it before anything else.

4. Overestimating discipline and underestimating triggers.

People assume they can “just spend less” without changing their environment. The quadrants expose patterns, like late night buying or weekend splurges, so you can set limits that match your real behavior instead of your ideal behavior.

5. Letting subscriptions hide in the wrong quadrant.

Streaming, apps, memberships, delivery services. These often blend into Essentials by accident, but many belong in Lifestyle or Impulse. Once you place them correctly, you can see which ones actually add value and which ones quietly drain your budget.

By organizing your money into four clear quadrants, you build natural guardrails. These guardrails stop silent leaks, keep your habits honest, and make sure your money supports your goals instead of slipping away.

5: What Happens When You Actually Apply the Quadrant System

Once you start using the 4-Quadrant System, certain shifts happen almost automatically. You stop guessing, you stop stressing, and you start seeing your money with sharp clarity. The system shows you patterns you could not see before and gives you structure that keeps you steady.

1. You gain instant clarity on your money habits.

The moment you place your spending into the four quadrants, the picture becomes clear. You spot leaks you never noticed. You recognize where emotion influences your choices. You see which habits support you and which ones drain you. Clarity alone changes how you move.

2. Your cash flow improves faster than you expect.

Impulse spending drops because it finally has boundaries. Savings rise because you prioritize them instead of hoping something is left over. Even if your income stays the same, your money starts working better because the system directs it with purpose.

3. You feel more in control with less effort.

You no longer argue with yourself about every purchase. You simply place it in the right quadrant and keep moving. The structure removes the mental load that makes budgeting exhausting. Decisions get easier because the quadrants guide you.

4. Lifestyle spending becomes enjoyable instead of stressful.

Fun purchases stop feeling like mistakes. You set limits, stay inside them, and enjoy the things you love without guilt. The quadrant gives you permission and boundaries at the same time, which is the sweet spot most people never find on their own.

5. You build real long term stability.

Savings grow consistently. Debt drops steadily. Your emergency fund stops being a “someday” goal and becomes a real buffer. The small wins stack up month after month until you look back and realize your entire financial foundation changed.

These results are not rare. They are what happens when you use a system built for real behavior, clear categories, and simple rules. Apply the 4-Quadrant System with honesty and consistency, and your money starts working for you instead of against you.

Conclusion

When you have a system, money stops feeling chaotic. You know where every dollar goes, what it supports, and how it fits into your life. The 4-Quadrant System gives you that freedom. It turns messy habits into clear patterns and replaces stress with structure. You make decisions with confidence because the framework does the heavy lifting.

If you want to feel that kind of control, start today. Begin with Step 1, The Audit. Look at your last 30 days of spending and place every purchase into a quadrant. That one action will show you more about your money than the past year of guessing.

Use the Quadrant System throughout this website as your guide. Once you commit to it, your entire financial life becomes easier to manage and a lot more predictable.